Yes, there is enough affordable housing

It's just not where enough people want to live.

There is plenty of affordable housing. It’s just not co-located with where it is needed. Smaller cities and towns, often in the South or Midwest, are quite affordable by accepted ratios of income to housing costs, even accounting for lower incomes in those areas.

In the context of housing, “affordable” is a relatively new term. We used to use labels such as public housing, subsidized housing, and low-income housing. The latest version might be called extortion housing—when cities tell private developers they must offer some proportion of proposed units at below market rates to get permits to build anything.

Now, my use of “extortion” might lead you to believe I am against this. I’m not completely. I do, however, propose that we recognize that when a developer must sell or rent some units at less than their cost plus usual profit, that results in the remaining market rate units having to be priced slightly higher to make up the difference.1 They become slightly less affordable. The market rate buyers rather than taxpayers cover the subsidy. At the margin, that could make a unit that would otherwise have been affordable to some buyers or renters now unaffordable.2

My expectation is that there will never be enough affordable housing—at least not where it’s wanted.

What does “affordable” even mean? A Maserati is not affordable for me, but it is for some people. What is affordable housing? Affordable for a single parent working at a minimum wage job? Affordable for a recent college graduate in her entry-level job? To a couple of a teacher and a police officer with a $150,000 income and two children? Affordable in Boston? In Platt City, MO? In Palo Alto, CA?

The U.S. Department of Housing and Urban Development (HUD) is the primary arbiter of affordability. From there, states and local jurisdictions may make adjustments. HUD defines affordable housing as

housing on which the occupant is paying no more than 30 percent of gross income for housing costs, including utilities. Keeping housing costs below 30 percent of income is intended to ensure that households have enough money to pay for other nondiscretionary costs….

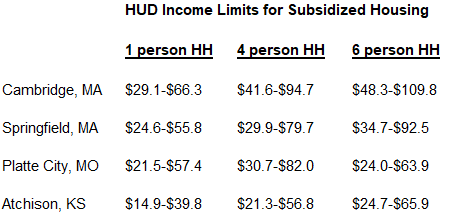

The income limits considered “affordable” vary for different federal programs. Cities may apply the HUD standards or set their own for local programs, such as for private development “extortion” side-aside units. They also are impacted by household size. For example, in Massachusetts, a family of four qualified for a Section 8 housing voucher (to be used toward rent) can earn as much as $94,700 in high-cost Cambridge or $79,700 in lower-cost Springfield (both are 80% of median household income in those areas). For some public housing programs, households qualify with up to 30% of the median income, the lower figures in the table below.

Gross income, of course, varies by region and within regions. In Atchison, KS, a city of 11,000 50 miles northwest of Kansas City, the median household income is about $55,000. In Cambridge, Mass., a city of 118,000 hard by Boston, the median income is $121,000.

Stick with me here: lots of numbers follow

A rule of thumb is that the purchase price of a house should stay within three to five times the household income. That would be $165,000 to $275,00 in Athchson, where the median price of houses listed is currently $175,000, or 3.2 times household income. In Cambridge, the recommended range would be $363,000 to $605,000, though the current median price of a condominium is $898,000 and a single-family house $1.9 million. The condo is 7.4 times the median income, and a house is 15.7 times income. And highlights the problem. Despite a median income in Cambridge 120% higher than in Atchison, in relative terms, a home (and, by extension, rent) is more than twice as much in Cambridge.

Thus, it is not surprising that there is so much talk about the need for affordable housing in Cambridge, Boston, and other cities with similar incomes and housing cost disparities.

Yet there are widespread areas with affordable housing. The most affordable housing states include Mississippi, Alabama, Kentucky, Oklahoma, South Dakota, North Dakota, Louisiana, and Iowa. Nevertheless, while many cities and small towns offer affordability, they also may offer fewer job prospects and fewer amenities than the most popular cities and are close in suburbs. Among large cities known for housing affordability are Detroit, El Paso, Memphis, Milwaukee, Tucson, Indianapolis, Oklahoma City, and Louisville.

Now, each of these cities has much to recommend them. The reality is that in affordable cities, housing supply is sufficient to meet housing demand. On the other hand, the least affordable cities include San Jose, San Francisco, Los Angeles, San Diego, Honolulu, Seattle, Boston, and New York. These are all cities, to be perfectly trite, “where the action is.” Or where many people think it is. Specifically, for jobs in technology, finance, academics, and research, there is more opportunity there than in the many more affordable cities. With this, I have provided no great insight, just reinforcement.

At this point, economics comes into play. If demand exceeds supply, market forces push up prices. In my post, “Affordable housing is not just a supply problem,” last September, I looked at the less examined demand side of housing, noting how housing formation has far exceeded population growth in the past 50 years.

Much of this increase in households is the result of changing social norms. Again, traditionally, children lived in their parent’s homes until they married, which in 1960 was about 20 for women and 23 for men. By 2022, that had risen to 30 for men and 28 for women.

And a large percentage of those still unmarried young adults are out forming households, with roommates or solo. Indeed, in 1960, 13% of households consisted of a single person. Today, it exceeds more than twice that proportion, 28%. Hence, more demand for dwelling units.

Moreover, the number of single-parent households nearly quintupled between 1960 and 2022 and more than doubled proportionally to the total number of households.

On the more often examined supply side, building to meet demand in the places where it is most needed is limited by the confluence of multiple barriers:

Land Costs: Land prices in urban areas are high, making it challenging to develop affordable housing. Developers often prioritize more profitable ventures. Unlike some smaller or newer cities, there is little to no land for development in older East Coast and some West Coast cities.

Zoning Regulations: Stringent zoning laws can hinder the construction of affordable housing. Some areas restrict density or mandate expensive design features. My city of Cambridge is in the midst of a discussion on whether to change zoning to allow taller residential buildings in low-rise residential areas.

And zoning changes bump into NIMBYism: “Not In My Backyard” sentiments that lead to resistance against housing projects that might lower property values as well as change neighborhood character. Such concerns can not be glibly dismissed. Some of the characteristics of neighborhoods that make them attractive in the first place, such as tree-lined streets with single-family houses, would be erased by tall apartments that cast shadows over their neighbors ’s homes.

Stringent building codes and regulations. City demand for increasingly changing stringent building codes and energy efficiency increases legal fees, architect and engineering costs, and land carrying costs during the often years-long permitting process.

Lack of Incentives: Developers may not find it financially viable to build affordable housing without government incentives or subsidies.

Avoiding these barriers is a challenge, but some may be mitigated. For example, several developers are starting to find that by using totally private funds rather than replying on various federal, state, or local funding programs, they can build faster and at substantially lower costs, resulting in even lower rents.

California has some of the highest-cost cities and the greatest need for affordable housing. In 2016, voters in Los Angeles approved a $1.2 billion bond issue to build 4,500 apartments for low-income people at a cost of $600,000 each. However, by forgoing government assistance and the many regulations and requirements, a private developer is self-financing a 49-unit apartment building at a cost per unit of $291,000—under half the government fund cost.

As reported in a recent Wall Street Journal article, a study commissioned by the city of San Jose found that affordable housing projects that received tax credits cost an average of around $939,000 a unit to build last year.

Publicly funded affordable housing must typically be built with labor agreements that dictate construction wages and working conditions, as well as energy-efficiency standards. Funding often comes from a variety of agencies, each of which has its own set of approvals and regulations that can slow construction and add to costs.

With private financing, “You’re cutting out millions of dollars just in soft costs,” said David Grunwald, an executive at RMG Housing, which is developing the SDS fund’s projects.

Can we subsidize our way to affordable housing?

There is somewhat of a circularity in trying to build our way into lower housing costs. Right now, there are more people who want to live in Cambridge or San Fransisco or New York than can afford to do so. In many cases, they settle for less expensive suburbs or cities. If we create more affordable housing—either by public or private subsidies— would that encourage more people to join the figurative “waiting list” of people who want to move in, in effect sustaining the demand for housing even as more is added? Building more subsidized housing in popular places would attract more who want to live there. It’s never ending. There will not be enough supply to meet increasing demand.

I mentioned at the start that a Maserati is not affordable to me. I’m thus not in the market for one. But what if, by government mandate, Maserati was required to sell 20% of its output at a price that would be affordable to me—and likely many others? The demand for these affordable Maeratis would balloon even as the manufacturer tries to make more with its limited resources. So would a actual waiting list grow—stretching our perhaps decades? I’m not implying that a fancy car is equivalent to the basic need for decent housing. However, the economic principle would be similar—demand fostered by an artificially low price would continue to outstrip supply.

Is building higher and denser the answer? Or encouraging urban sprawl?

Housing advocates in Cambridge are pushing for zoning changes that would encourage building up, given that the six square miles of the city have virtually no room to build out. Proposals are being made to allow six, 12, or even 15-story buildings where there are now three-story homes and five-story apartments. A similar solution is inevitable to be proposed in any city that is already densely inhabited. In other cases where land is available, there is the conundrum of spawl, resulting in longer commutes and more traffic.

Cities often work at cross purposes, lamenting the high cost of housing while laying on municipal spending, thus pushing up real estate taxes, which, after all, are part of housing costs. Every increase moves housing from affordable to unaffordable for a few more people.

My solution. Not.

When most offices went virtual during the pandemic, we found that large numbers of folks from high-cost cities in California, New York, and New Jersey relocated to Idaho, Vermont, Maine, and Delaware. Some employers learned that remote employees could get the job done without the need for costly office space. So, there’s that confluence of market forces with technology. However, there are many jobs that do not lend themselves to relocation. And, long term, the population will continue to grow.3

The resolution, if any, is most likely to emerge from a combination of small changes and fixes, such as living in smaller—and thus less costly— spaces. Over time, perhaps high housing costs will encourage more younger people to stay in their parents' homes longer, as was typical until the latter part of the last century. Existing and new government programs will continue. Market forces may encourage more employers and, thus, those seeking housing, to find it in the cities where affordability is not a problem. We have the housing supply. We need to somehow disperse the demand.

I suppose some readers of a progressive bent may counter that the developer should eat the lower revenue and accept a lower profit. But if we want to encourage developers to risk their capital—many have failed—they must be allowed to aim for a return that encourages them to engage in the often long and expensive process of housing development.

For example, suppose a family figured that if it really skimped, it could stretch its budget to pay $2000 a month in rent. They find a new development they liked, which was required to set aside 20% of its units for a local “affordable” program. Market conditions would have dictated $2000 for this apartment. However, because it had to price some units below market, at, say $1800, the remaining units were priced at $2150 per month, making it out of that family’s price range.

Unless Donald Trump is re-elected and follows through on his threat to report all undocumented immigrants as well as lock down the border to all—except maybe Norwegians.

I'll contribute $5.00 to your Maserati fund. Yesterday, The NY Times published an article describing the use of modular homes in Sweden to address the housing affordability crisis. Along with rethinking and reducing the regulatory/zoning impediments, would Sweden's modular experiment be replicable in the US?

Susan hit the nail on the head. One other factor not included is the cost of money is when HUD builds housing. Often they have 40 year fixed rate mortgages that are significantly below market rate monthly payment schedules. The big national housing developers rarely build in cities.

One other cost issue is parking. Building underground spaces in the Boston area cost at least $75,000. Many over $100K. Current parking spaces in Back Bay and Beacon Hill have been reported to be as high as $500K. Far more than your imagined Maserati.